Car

Best Time to Buy a Car in India 2025: Festive Season + GST Cuts

CarPhD

Car

The Navratri festival of 2025 will be remembered in India’s auto industry as a watershed moment. Carmakers, dealerships, and auto platforms witnessed extraordinary demand, with deliveries, bookings, and enquiries scaling to new highs. At the heart of this surge was GST 2.0—the sweeping tax reform that restructured vehicle taxation, enabling automakers to pass on relief and stoke consumer momentum.

GST 2.0: The Structural Shift in Auto Taxation

To grasp why demand exploded, one must understand the GST changes and their impact on vehicle pricing.

• Under GST 2.0, the earlier multiplicity of slabs (5 %, 12 %, 18 %, 28 % + cess) has been rationalized and the additional cesses eliminated.

• Small cars (petrol ≤ 1,200 cc, length ≤ 4 m; diesel ≤ 1,500 cc) now fall under 18 % GST (down from effective rates of ~28 % + cess) — delivering a sharp cut in tax burden.

• For luxury cars and large SUVs, though the applied GST rate is steeper (40 %), the removal of cesses means that the net tax burden is lower than in the prior system.

• Component taxes are unified at 18 % across product lines, easing compliance for OEMs and reducing cost unpredictability.

In short: GST 2.0 removed a major distortion (the cess) and enabled genuine tax relief for both mass-market and premium vehicles.

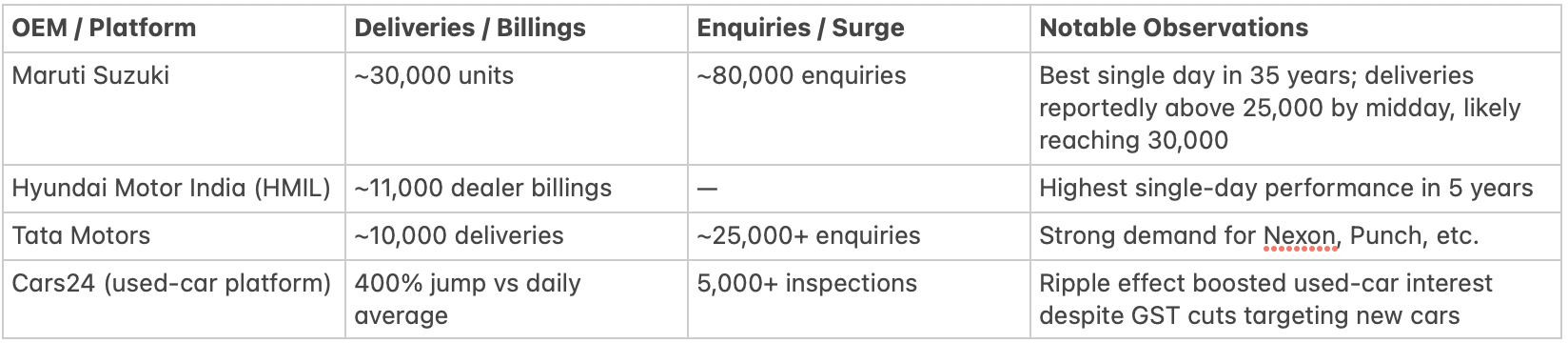

Navratri Day 1: The Surge in Numbers

The opening day of Navratri (coinciding with the rollout of GST 2.0) witnessed a rush of demand. Key headline figures:

These numbers represent multiples of what the sector usually sees in a non-festive day — in some cases 5–6× normal volumes.

Maruti itself disclosed that even before Navratri, since September 18 (when new/adjusted prices were announced), it had been receiving 15,000 bookings per day — about 50 % above its typical run rate.

⸻

OEM-Wise Highlights & Model Impact

Maruti Suzuki

• Price cuts of up to ₹1.29 lakh across its lineup (models: Alto, Swift, Brezza, etc.) in response to GST relief.

• Small car inquiries jumped ~50 %.

• Some dealers reportedly warned of stock-outs for specific variants.

Hyundai

• Passed on full benefits of GST rate cuts.

• Focus on compact & mid-SUV models saw the highest drift in bookings. (Implied via reports of demand skew)

Tata Motors

• Strong interest in the Nexon, Punch, and mid-SUV segments.

• Price cuts and festive discount stacking (up to ₹2 lakh in some cases) plus full GST pass-through.

Honda

• Honda India cut prices of Amaze, Elevate, City by as much as ₹1.2 lakh in wake of GST reforms.

• This made these models more competitive in compact / mid-sedan / SUV space.

Other OEMs such as Mahindra, Kia, Skoda, Toyota also followed suit with price cuts and discount stacking, especially for models falling within the sub-4-metre / ≤1,200 cc bracket.

⸻

What’s Driving the Surge (Beyond Tax Cuts)

While GST 2.0 was the spark, several reinforcing factors amplified the demand:

1. Pent-up Demand Deferred by ‘Shradh’ Period

The timing coincided with the end of the 16-day ‘Shradh’ period, during which many buyers avoid big purchases. Navratri’s opening offered a culturally auspicious window.

2. Festive Psychology and Consumer Confidence

The symbolic launch of a cleaner, simpler GST aligned with the festival’s mood of renewal and auspicious beginnings. Many buyers viewed the tax cuts as a “government-driven discount.”

3. Aggressive Financing and Dealer Incentives

OEMs and financiers offered sub-8 % interest rates, zero-processing fee offers, flexible down payments, and extended warranties — all stacking with GST relief. (Reported in media commentaries)

4. Improved Inventory Flow & Interstate Logistics

With inter-state taxation hassles reduced under GST 2.0, OEMs could redistribute inventory more flexibly, reducing stock-outs in tier-2 and tier-3 markets.

5. Ripple Effect on Used Cars

Rising interest in new cars increases trade-ins, inspections, and resale inquiries—hence the surge in used-car platforms. As Cars24 reported, a 400 % jump in deliveries by early afternoon.

⸻

Market Share Shifts (Preliminary Signals)

It is early to draw definitive conclusions, but some emerging patterns are worth noting:

• Maruti Suzuki’s strong volume delivery gives it further cushion to defend or even expand market share in compact car / entry segments.

• Tata Motors, with aggressive discounting and full pass-through, may gain share in compact SUVs and crossover segments.

• Hyundai stands to benefit in the mid-SUV and premium compact segments, leveraging its brand and model range.

• OEMs that delayed or partially passed on GST gains may see a relative decline in momentum, especially in price-sensitive markets.

⸻

Risks & Cautions

• Sustaining the momentum over the full festive season (Diwali, year-end) will be crucial — a one-day rush is not enough.

• States may push back on revenue implications of cess removal; fiscal pressures could lead to state-level surcharges.

• Global supply chain constraints or semiconductor shortages can create bottlenecks if demand stays elevated.

⸻

Outlook: The Road Ahead

If the Navratri Day 1 trend is any indicator, FY26 is shaping up to be among India’s strongest automotive years. Analysts are adjusting forecasts upward, factoring in a 10–15 % volume boost in Q4 (~Oct–Dec).

Car OEMs have already ramped up production, extended shifts, and scaled supply chain buffers. The combination of policy-led tax relief, festive timing, and revived consumer confidence has created rare alignment.

GST 2.0’s structural reform has shown that the tax system itself can act as a demand stimulus—especially in a price-sensitive market like India’s auto sector. If that stimulus can be sustained (and managed on the fiscal side), this era may come to be seen as a turning point in India’s automobile growth story.